Inventory is hands-down the most critical aspect of any business. You need to have a substantial inventory in place and only then can you think of marketing, selling, and shipping! As the task is crucial, it’s maintenance also requires effort and an eye for detail. Without inventory management, your store is bound to face losses down the road. To know how you can successfully manage your inventory and optimize your process always – carry on!

What is Inventory management?

Inventory management is the process of keeping a track on the inventory of a business. It includes stocking, tracking, analysis and prediction of future sales demand for the products sold by the company.

Inventory management is a continuous process and can be affected by many external factors like the economic status of the country, public demand, time of the year, etc. Along with this, the internal factors involved include the size of your warehouse, relationship with your supplier and the available capital you have for keeping up with the inventory.

Here are some tasks you need to do to make sure your inventory management is carried out seamlessly.

1) Continuously track stock levels

2) Analyze the cost of stock and find better options at intervals

3) Analyze shipping and handling costs

4) Look for ideal warehouse locations

5) Analyze past sales data

6) Predict future demand

7) Determining when to replenish and how much is needed

Inventory Management Strategies

1) FIFO

FIFO refers to First in first out. This method implies that the customer always gets the freshest inventory. It also helps in maintaining a uniform flow and holds the freshness of the product. Thus, it is more suitable for perishable goods.

2) FILO

FILO refers to First in last out. According to FILO, the product which enters first is the last one to be sent out. It can be useful for some products but is mostly unused these days.

3) Minimum Viable Stock

These are the minimum stock levels your inventory must contain. Thus, if your levels fall below these limits, it is a call to purchase fresh stock…

4) JIT

JIT means Just in time inventory. Here, you can order your inventory as and when you receive your order. Suitable for people who import products and don’t want to block their budget on the inventory. But this method can also be time-consuming.

Calculating Inventory

Calculating inventory is a critical yet necessary task for any eCommerce business. You can only do so by analyzing past sales and predicting future demands. For doing so, you need adequate data and inventory tracking. You can do so by using excel, but that method is outdated and extremely time-consuming. Thus, making use of robust inventory management software can be a boon.

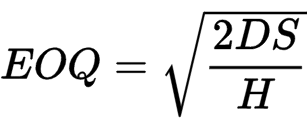

After analyzing and assessing your data, you need to follow a set rule to calculate the best estimate for buying inventory. To do so, you can use your data from past sales and apply it to the economic order quantity formula(EOQ).

The EOQ is dependent on three variables:

1) D -Annual demand quantity

2) S – Static (fixed) cost per order

3) H – Carrying cost/Holding cost per unit

Using this formula, you can calculate an ideal quantity for your product and place an order suitably.

Things to Keep In Mind

1) Remain organized

At all times, make sure your inventory is in order and updated. This practice saves you a lot of time while placing orders. Your storage house must be designed in a manner that all the products are visually traceable and accessible for everyone.

2) Keep a check on your inventory at all times

If you follow FIFO, designate time intervals to check and update inventory regularly. This strategy can help you stay stocked for the right amount of time without having to bear losses. But also, don’t overstuff your warehouse or order in excess. As sales don’t depend on just one factor, it can get difficult for you to get rid of extras and result in losses.

3) Make use of JIT

This process saves wastage of products. Only if you can forecast your sales based on previous data, you can make suitable predictions for this strategy. Follow this for efficient sale and reduced the cost of inventory management.

4) Forecast and improve

Never gamble with the numbers for the future and make a thoroughly informed forecast for your sales. Apply this forecast for purchasing inventory and operate efficiently. To improve forecasting, conduct market research, observe market demand models, analyze demand patterns and understand required stock levels.

Follow these few guidelines for inventory management and make sure to save thousands on your spends — an excellent way for managing expense at a grass-root level of the business.